There has been a lot of excitement about the promise of wholesale distributed generation in California in recent years. But the state still hasn't lived up to its promise.

Wholesale distributed generation (DG) refers to front-of-meter systems (typically sized between 1 megawatt and 20 megawatts) that sell power directly to the utility or a third-party offtaker. This is an important market niche that remains underdeveloped. But there are some reasons to be optimistic about the future of wholesale DG in California -- if some key policy changes can be made.

I’ve written various columns over the years for GTM highlighting the opportunities, innovations and issues facing distributed generation. Last year, I wrote a very optimistic piece that reflected my excitement over the California Public Utilities Commission's push for more DG. In particular, I highlighted the new Distribution Resource Plan proceeding and the new interconnection maps that utilities were required to produce as part of their DRPs.

GTM's Stephen Lacey recently wrote a piece kicking off a series of articles on the utility of the future. In it, he said: “Today, experts across the energy industry are predicting a…shift toward a decentralized, digital and dynamic grid system.” I agree with his appraisal of this trend. But California -- long considered the leader on these issues -- has yet to address a number of hurdles that stand in the way of realizing that future.

In fact, the obstacles now facing solar DG in PG&E’s territory threaten to kill this niche entirely.

Interconnection and procurement are the key hurdles facing wholesale DG

As has been the case for a long time, the key issues with respect to distributed energy resources (DER, which includes DG as well as electric vehicles, energy efficiency, energy storage and demand response) are interconnection and procurement. Interconnection permission is required for all types of DERs except for energy efficiency and demand response. Everything else -- solar, wind, biomass, geothermal, small hydro, electric vehicles and energy storage -- requires interconnection permission from the utility. This can be and usually is a rather lengthy and expensive process.

So interconnection is the first and foremost issue to be resolved when looking at how to promote DER. If you can’t affordably interconnect DER then those resources won’t be developed.

Procurement refers to the ability to sell power to a customer, whether that’s the utility or not. The main path to success since direct access was shut down in California in 2001 has been selling to the utility to help meet their renewable energy goals. While there have been a number of programs for utility procurement of DER in recent years, very few have been effective, and it seems that the political will and vision have been lacking in terms of creating procurement programs at the scale required. But first let’s look at interconnection in more detail.

Interconnection hurdles

The new utility interconnection maps include "Integration Capacity Analysis” (ICA) figures that attempt to show how many megawatts of DERs can be interconnected at any given circuit location. The ICA figures use a new methodology focused on showing what can be interconnected without substantial grid upgrades, with the idea being that it is good to know what can be interconnected on specific circuits without major expenditures on upgrades.

This change appeared to be a major improvement over the existing interconnection maps because the existing maps focused on the 15 percent of peak load limit that is a key screen (Screen M) under the Rule 21 interconnection tariff. The ICA figures are higher than the 15 percent Rule 21 figures, which, all else equal, is a good thing.

After working with the new maps over the last six months, however, I’ve come to realize that what appeared to be a major step forward may be a step backward, at least for now. This is the case because the ICA figures don’t reflect how the current Fast Track interconnection process works. The point of the new ICA methodology was to use a different set of screens to improve estimates of what can be interconnected affordably.

If DERs can’t interconnect to the grid under Fast Track, the vast majority of DER projects won't be able to interconnect at all and they will stall. (Again, energy efficiency and demand response don’t need interconnection authority, so my use of "DERs" from this point on should be understood to exclude these two technologies.)

So until the Fast Track interconnection process is modified to reflect the new ICA methodology (which should happen as soon as possible), the ICA figures in the new maps are purely theoretical. No DERs will be using detailed study interconnection procedures, because those procedures are far too expensive and take far too long.

For example, under the Independent Study Procedure, one of the two types of detailed study processes, the Phase 1 study fee for a 3-megawatt solar project is $10,000 -- plus $15,000 for Phase 2, plus engineering fees of at least $15,000, and legal fees that will probably be another $10,000 at the least.

It could cost a developer $50,000 just to learn what it will cost that 3-megawatt project to interconnect at that location. This may have to be done a number of times if the locations chosen can’t support the planned capacity.

The comparable fees under Fast Track are $3,300 for the initial and supplemental reviews, rather than the $25,000 just described for the Phase 1 and 2 studies. Moreover, the Fast Track process takes six to nine months, typically, and the detailed study process can take 12 to 36 months, with the longer timeframe sometimes being required for the cluster study process. The cluster study process is the second and most demanding type of detailed study process. The study fee alone is $50,000, plus $1,000 per megawatt.

We have good data showing that DG must use Fast Track to interconnect. For example, PG&E’s interconnection queue of over 10,000 DG projects over the last few years shows that only one project under 10 megawatts has successfully interconnected under the cluster study process. The vast majority have used Fast Track, and some have used the Independent Study Process, which is the less expensive and less time-consuming alternative to the cluster study process.

In practice, this means that the ICA data on the new interconnection maps will provide figures up to twice as much as what can actually be interconnected affordably under Fast Track. This is why the new ICA figures are misleading about which DERs can be interconnected affordably. Until the Fast Track process is amended to reflect the ICA screens, this will continue to be the case.

A simple fix for this issue is to return the maps to the Rule 21 data as the default and only make the ICA data the default once Rule 21 has been reformed to reflect the ICA methodology. This will be a major improvement. But that improvement will be realized in practice only when Rule 21 is reformed.

Thinking a little further ahead, if state policymakers really want to boost wholesale DG, they should work diligently with the utilities to create a “click-and-claim” option in the interconnection maps. This will allow developers to see how much capacity is available on any given circuit and to claim that capacity simply by clicking on a button in the map. (I’ve described this click-and-claim process in more detail here and here.) These improvements will bring the interconnection process into the information age where it belongs.

The irony now is that PG&E and Southern California Edison are more eager to implement these new options than is the CPUC itself, because the commission is engaged in a very extended 8-year reform process under the DRP initiative. With a focus on reforms in the near term, this process should only take a couple of years.

Procurement hurdles for DG

The second major hurdle for a robust DG market is procurement. The CPUC’s DRP process is addressing this issue by creating a new “locational net benefits” methodology that would value the grid benefits provided by the various types of DER and (presumably) identify ways in which this value would be captured in sales contracts. It’s still very early in this process, so we can’t know at this point how it will unfold.

The locational benefits analysis could be a significant boon for DG and DERs, but it will depend heavily on the numbers that come out of the new process and the ways in which this value can be captured in sales contracts.

A promising related initiative is the campaign by the Clean Coalition, an environmental nonprofit based in the Bay Area (and one of my clients), to reform the Transmission Access Charge (TAC) in a way that would allow wholesale DG to obtain payments of about 3 cents per kilowatt-hour based on the fact that they don’t require any transmission access. If this amount, or something near this amount, is ultimately approved for DG compensation, it would be a major boost.

Positive locational benefits could do much to mitigate what has become an increasingly serious problem for DG: a major shift in the time-of-delivery value for solar. Time-of-delivery (TOD) adjustments exist to encourage (or discourage) generation when it’s needed the most (or least).

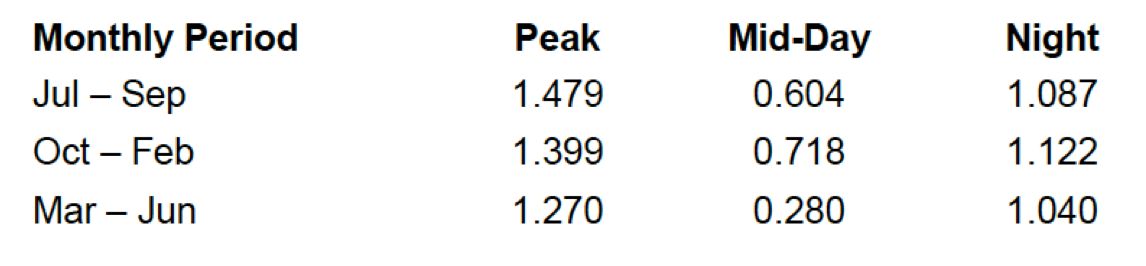

For example, PG&E’s peak demand period is now from 4 p.m. until 9 p.m., having shifted from an early afternoon peak to an evening peak. TOD adjustments used to give a substantial boost (about 25 percent) to solar projects, due to the much earlier peak period. But now that parts of the state are awash in new large-scale and rooftop solar, the TOD tables have been steadily adjusted such that they now significantly penalize new solar projects.

PG&E’s 2016 average midday TOD adjustment, for example, which affects solar projects the most, is now a whopping minus 42 percent (as a weighted average) over the headline PPA price. And at times, it provides a 72 percent deduction from the base PPA price (midday from March until June).

This means, for example, that a base PPA price of 10 cents per kilowatt-hour is reduced to just 2.8 cents per kilowatt-hour during this three-month time period. And the average reduction for solar is to about 5.8 cents per kilowatt-hour, down from 10 cents per kilowatt-hour in our hypothetical base price.

PG&E’s new TOD table essentially kills new solar projects. The figure below outlines PG&E’s 2016 TOD rates for projects under the standard Renewable Market Adjusting Tariff (Re-MAT).

SCE’s 2016 TOD adjustments are much different from PG&E's. The peak time begins at 2 p.m. rather than 5 p.m., and the 2016 figures result in a 5 percent increase for shoulder production and a 24 percent increase during the peak demand period.

These figures reflect differences in system needs between the two big utilities, not any kind of conspiracy by PG&E to harm solar. Regardless of the cause, however, the fact remains that new solar is now completely unviable in PG&E territory at the prices currently offered under Re-MAT and related programs.

More robust procurement opportunities need to be offered for DER. The locational benefits analysis will not address this longstanding issue, even if it does lead to more fair pricing for DER.

The legislature and regulators have been experimenting with new DG procurement programs in recent years, but they haven't gone all-in on new procurement efforts in this important niche.

The pattern has been to offer a pilot program, then modify a little and try that new approach, then offer something different on a pilot basis again and see if that works. Normally, this kind of experimentation would be smart policy. But when it comes to DG procurement, we already know pretty well what works and what doesn’t.

We know that feed-in tariffs work very well in many jurisdictions around the world, including here in California. And yet the term “feed-in tariff” has practically been blacklisted in recent years because of misperceptions that feed-in tariffs must offer above-market prices. They don’t, and historically they haven’t in the United States. Rather, avoided costs have generally been used to set feed-in tariff rates in the U.S.

Wholesale DG has had a limited number of procurement opportunities over the last decade.

In 2006, California established a feed-in tariff program (AB 1969) for all types of renewables with a 250 MW cap. The price was set at the “market price referent,” which was a type of avoided-cost calculation that used a 500-megawatt natural-gas plant as the default power price comparison. So all projects procured under AB 1969 were by definition cost-effective.

This program was modified by SB 32 in 2009 to expand the size to 3 megawatts and allowed environmental benefits to be included in the price paid to developers. While this law was passed to allow for additional grid benefits to be priced into the contract, in practice the CPUC used the additional flexibility to reduce the price paid when it created the Renewable Energy Market Adjusting Tariff price mechanism that is still in place today -- contrary to its own staff recommendations.

This is now the default program for projects sized at 3 megawatts and below. It eliminates certainty about the contract price until the contract is actually obtained (because the contract price adjusts up and down based on interest by developers); it creates a race to the bottom in terms of pricing reductions; and it's hard to know how long it will take to obtain a contract once a developer is in the queue. As discussed above, a major new problem with this program is PG&E’s extremely harmful TOD adjustments for solar projects.

California also experimented with a small program for wholesale DG solar projects with the utility solar PV programs approved in 2009 and 2010. The utilities originally requested authority to procure and own 250 megawatts of solar projects. The CPUC approved their request, but mandated that 250 megawatts of solar be owned by third parties, expanding the market further.

Some of these megawatts have been procured, but much of the program ended up being rolled into Re-MAT or the Renewable Auction Mechanism (RAM) after utility requests to basically kill these solar programs. To my knowledge, only 150 megawatts of the utility-owned solar projects were ever built (by PG&E), and it’s still not clear what happened. PG&E’s share of this program was arguably not DG because it focused on projects up to 20 megawatts. SCE’s program focused on rooftop projects 2 megawatts and below, as did SDG&E’s.

California’s latest program is the Green Tariff Shared Renewables (SB 43) program, which just went live. This allows utility customers to sign up for 100 percent renewable energy and offer contracts to third parties. The megawatts will be procured under either Re-MAT or RAM, so there’s no new procurement mechanism associated with this program. It’s too early say how much of the 600 megawatts authorized under SB 43 will be procured under this new program. But since Re-MAT is the procurement mechanism for some of the program, we already know that there is a great deal of room for improvement.

The new Distribution Resource Plan proceeding created by AB 327 is not considering procurement beyond the locational benefits analysis described above, despite some parties calling for including procurement.

I’m not including the RAM here, because it’s for projects up to 20 megawatts and doesn’t require that projects be connected to the distribution grid.

In sum, we have a decade of failed experiments in the wholesale DG space, and we are badly in need of a serious program that can scale. We now have an abundant track record of what works and what doesn’t work. A revised Re-MAT program scaled up to a reasonable size is the most obvious fix, but it should be made a true feed-in tariff, with the price set at avoided costs to ensure no net cost to ratepayers and some price certainty for developers.

It seems that we’ll need legislative action on procurement. In this election year, that also seems unlikely, even with the cost-effectiveness requirements just described.

I don’t want to paint an overly negative picture of the prospects for wholesale DG or for DER more generally. Even with PG&E’s horrendous new TOD table, there is some hope for solar in other IOU territories, and for other types of DG (like wind or biomass) in all IOU territories.

There is much reason for optimism given the general trends in California and around the world. But for California to maintain its position of leadership in the U.S. on these issues, and to develop the DER niche to its full potential, much work remains to be done.

The interconnection issues facing DERs can be resolved under current regulatory processes if the CPUC is willing. The procurement issues are a larger hurdle, and will require some serious leadership in the legislature and the CPUC to create appropriately-scaled new procurement efforts and to fix the failures of the current programs.

Resolving these issues will require steady help and vigilance from those who care about this space.

***

Tam Hunt is a lawyer and owner of Community Renewable Solutions LLC, a renewable energy project development and policy advocacy firm based in Santa Barbara, California and Hilo, Hawaii, co-founder of Solar Trains LLC, and author of the new book, Solar: Why Our Energy Future Is So Bright.

41

41

15

15

9

9