Over the past two and a half years, Hawaii has been embarking on the most aggressive effort in the United States to change the way utilities are financed by the public they serve, by leaving behind the capital expenditure-focused, “spend money to make money” paradigm of traditional cost-of-service regulations.

To replace it, Hawaii is looking toward performance-based ratemaking (PBR), a catch-all term that encompasses all kinds of regulatory structures. The common goal is to financially reward utilities for doing things regulators and policymakers have decided they need to do better and to stop rewarding them for things that end up costing customers more than they return in customer benefits.

For Hawaii, that PBR impetus is aimed at Hawaiian Electric, which operates investor-owned utilities on the islands of Oahu, Maui and Hawaii. On one hand, regulators want to limit customer rate increases, especially for large capital projects that may not align with the island state’s clean energy imperatives. They also want to remove the inherent bias for utility-owned projects that can serve as a disincentive for more creative approaches that tap customer-owned rooftop solar, behind-the-meter batteries, grid-responsive loads and electric vehicles.

On the other hand, they want to avoid putting the utility under a structure that could lead to excessive losses that might alienate Wall Street investors and dissuade lenders from supplying the capital the company needs. They also want to reward the utility for doing its core jobs more efficiently — and to boost those rewards when it exceeds state mandates to shift from centralized fossil-fueled power plants to a clean and decentralized energy future.

In December, the Hawaii Public Utilities Commission approved a decision and order that takes the next step in this journey. It’s the result of years of grinding negotiations and compromises between Hawaiian Electric (HECO) and business, environmental and consumer stakeholders, and it doesn’t incorporate all the PBR concepts laid out in the first phase of the effort.

But it does go much further than any of the PBR efforts underway in the rest of the U.S., according to participants in the process. That’s because it takes a vital, if still conceptual, step, beyond tinkering at the edges of the cost-of-service model, by setting a clear signal that, for HECO, there’s no going back to the old way of doing business.

“One of the hidden keys” to the PUC’s decision and order “is what they said about their long-term view of PBR,” said Isaac Moriwake, an attorney with Earthjustice representing the Blue Planet Foundation in the proceeding. He cited language throughout the document highlighting that the PUC views the five-year runtime of the new regulatory structure not as an “experiment that we will abandon” but rather as the starting point for a new way of doing business.

If the PUC holds to this commitment, it would mark a departure from the rest of the PBR efforts undertaken in other states over the past few decades, said Ron Binz, the former Colorado utility commissioner and regulatory expert representing Blue Planet in the proceeding.

“The basic plan of every utility was to fix everything with a capital expenditure because that brought long-term revenues,” he said. Other states have started these kinds of reforms, only to relapse to cost-of-service ratemaking at the end of them. Setting the expectation that this won’t happen in Hawaii is what "distinguishes this decision from many other decisions in the country.”

Jim Kelly, HECO’s vice president of corporate relations, concurred that the new framework puts the utility in a new situation. “We’ve helped develop a plan that looks strong on paper, but now comes the part where we have to make it work in real life,” he wrote in an email.

“We’re the ones who will have to work out the kinks, just as we did with the practical realities of delivering power safely and reliably with huge amounts of variable resources,” Kelly wrote, highlighting HECO’s challenge in meeting state mandates for zero-carbon energy by 2045 on an island that can’t rely on surrounding utilities and power grids to manage those disruptions. “How successful the experiment is will likely influence whether other jurisdictions and utilities move quickly or haltingly toward PBR.”

The multiyear rate plan: A clear exit from the capex-driven model

So how does Hawaii’s new model work? The first step is developing and implementing a multiyear rate plan, or MYRP — a model that’s been used in other states but not in the same form that Hawaii has chosen.

Hawaii’s five-year MYRP will replace the traditional three-year rate case, in which utilities ask regulators to approve capital and operational costs and revenue requirements, with a longer-term plan that comes with annual adjustments. Other states have allowed utilities to work under similar longer-range plans, but many of those have been criticized by ratepayer advocates for giving utilities too much leeway to increase costs and rates without adequate review. Recent attempts by utilities such as Duke Energy to secure MYRPs have failed to win political support as a result.

Hawaii’s new MYRP is different in that it sets tight limits on the annual rate increases HECO will be allowed and largely divorces them from rate-of-return on capital investments, said Murray Clay, president of the Ulupono Initiative, a impact investment firm that independently modeled the financial outcomes of the various revenue structures under consideration in the order.

HECO’s three operating utilities on Oahu, Maui and Hawaii will start with approved levels of revenue of about $660 million, $157 million and $155 million, respectively. Every year, those rates will be allowed to raise by an amount set by an “annual revenue adjustment” formula, set not by how much capital they’re investing but rather based on a complex calculation of their reasonable cost of doing business, plus a number of extraneous factors.

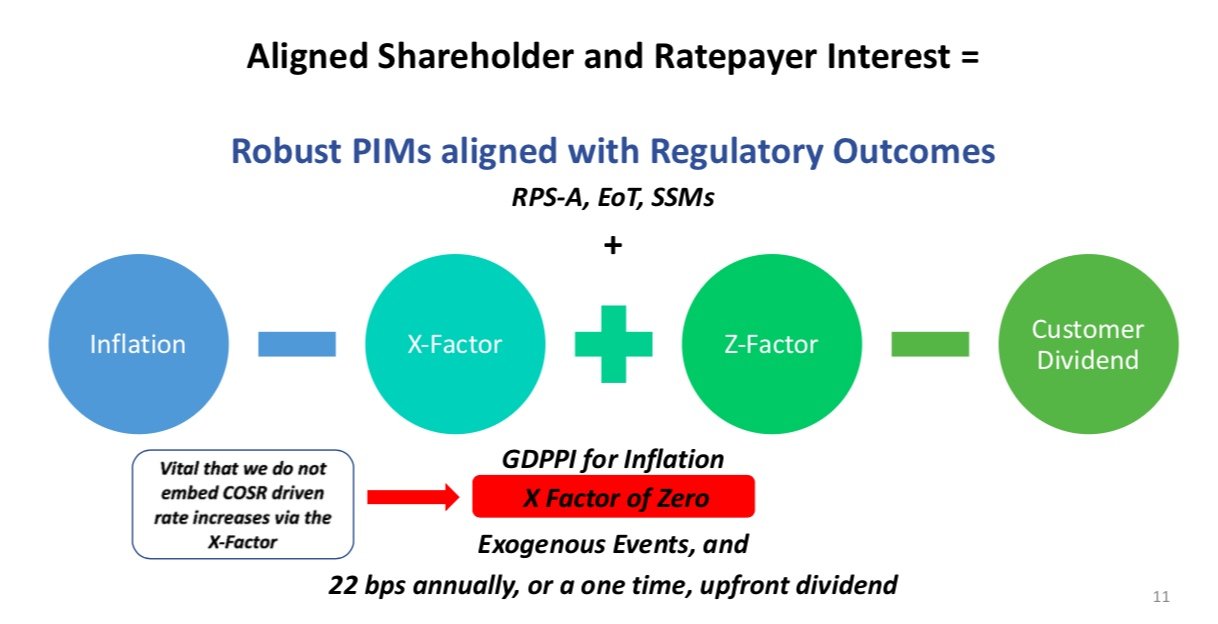

While the details are complex, the basic formula below captures the high-level factors, including a base rate increase accounting for inflation, an “x-factor” or “productivity factor” to account for the unique factors of operating a utility, a “z-factor” to account for unpredictable events like storm recovery or changes in tax liability, and a “customer dividend” that essentially works to reduce customer rate increases over time.

(Image courtesy of the Ulupono Initiative)

The main point, Clay said, is that “it doesn’t matter how much they spend or how little they spend — it goes up by this indexed amount each year. That means a utility can profit if they can find a way to cut costs. At the same time, if they’re wasteful, they don’t get to get it back.”

To be sure, the individual components of this formula were the subject of vigorous debate over their proper balance of protecting ratepayers from increases and protecting the utility from a financial straitjacket, he said. HECO argued that its productivity factor should be set at a negative rate rather than at zero because utility costs rise faster than inflation, for instance.

Not all utility costs are constrained by this formula. The costs of coal and oil shipped in to power HECO’s generators, which make up about 60 percent of utility costs, will remain pass-throughs on customers’ bills, Binz said.

And while about two-thirds of HECO’s capital costs will now be treated the same as its non-rate-baseable operational costs, the remaining third or so could be subject to recovery under the “exceptional project recovery mechanism,” or EPRM, Clay said. That’s the new name for a longstanding “major project interim recovery” allowance that lets HECO seek approval to recover rates for large-scale investments not part of its base rate case, which was last applied to its 50-megawatt biodiesel generator installed at the former Schofield Barracks U.S. Army base.

Unlike the capex-structured model, however, the EPRM will consider both capital and operational costs for rate recovery. That could allow HECO to consider alternatives to utility-owned infrastructure for major projects, such as the solar, battery and water heater installations being proposed as a “non-wires alternative” to building substations and circuits to serve a fast-growing community in west Oahu.

After much debate on how to bound the recovery structure of these future EPRM projects, the utility commission ended up “saying, basically, we’ll leave it up to our discretion,” Clay said. Some capital cost recovery may be prudent for work like extending electrical service to an area that now lacks it, he noted. “But at least now that there’s not this capital bias, the utility will have an incentive not to put forward just capital projects.”

Performance incentive mechanisms: Revenue tied to success or failure

If the multiyear rate plan sets a ceiling of sorts on how much rate recovery HECO can expect to rely on from year to year, the next step in the performance-based ratemaking journey is performance incentive mechanisms, which set the rules for how HECO can boost revenue by doing certain things better, faster or more efficiently.

PIMs offer a "carrot" for utilities, along with the "stick" of more traditional mandates for utilities to hit performance targets. These range from long-standing metrics such as power outage frequency and duration or customer service call response times, to energy efficiency spending or renewable portfolio standard (RPS) targets.

These kinds of compliance targets give utilities little incentive to do anything more than the bare minimum to hit them, however. Offering utilities incentives for exceeding targets could solve this problem — but such efforts have often run into opposition from consumer watchdogs worried that utilities will take advantage of them to raise rates.

This tug-of-war between incentives and ratepayer costs played out in Hawaii’s performance-based ratemaking debates as well and yielded a relatively narrow set of PIMs that stakeholders could agree on pursuing at this stage of the proceeding, Earthjustice’s Moriwake said. “It was so much effort just to get the foundations of the revenue mechanism" ironed out.

But they do include several important incentives for HECO to align its imperatives with the state’s clean energy goals, he said — most notably the new accelerated renewable portfolio standard, or RPS-A.

RPS-A: The country’s first affirmative utility incentive for renewable energy

Along with the existing $20 per megawatt-hour penalty to HECO for failing to meet its annual targets, which scale from 30 percent in 2020 to 40 percent in 2030, the RPS-A adds an incentive for exceeding them. That incentive adds up to $20 per megawatt-hour above its targets in 2021 and 2022, $15 per MWh in 2023 and 2024, and $10 per MWh thereafter through 2030.

According to Ulupono’s modeling, those incentives could add up to $10 million per year by 2025 “if they really push,” Clay said. If the RPS-A is extended, total revenue upside through 2030 could add up to as much as $172 million.

The new standard also adjusts the legal definition for calculating the RPS to ensure it accounts for Hawaii’s growing rooftop and distributed solar resources by measuring utility-scale renewables growth against total generation rather than net electricity sales, he noted.

HECO’s Kelly expressed qualified support for the RPS-A, noting it has “a lot of revenue potential over time.” But he also noted that “the outcomes aren’t completely under our control,” with third-party developers responsible for financing, site control, community engagement, permitting and construction.

At the same time, HECO is under pressure to install the solar, wind, batteries and grid investments needed to replace Oahu’s 180-megawatt AES coal plant, now set to close in 2022, as well as an oil-fired power plant on Maui set to close in 2024.

“If that plant were to go away with no renewable replacements, costs will go up, because HECO will have to fall back on its diesel plants,” Moriwake said — an outcome that could hurt the utility and customers alike.

All in all, this approach to an “affirmative incentive for renewable energy” stands out in a world of state-by-state RPS targets, he said. In fact, “I think this is going to be the very first PIM for renewable energy in the country.”

Finding the right targets for broader performance incentives

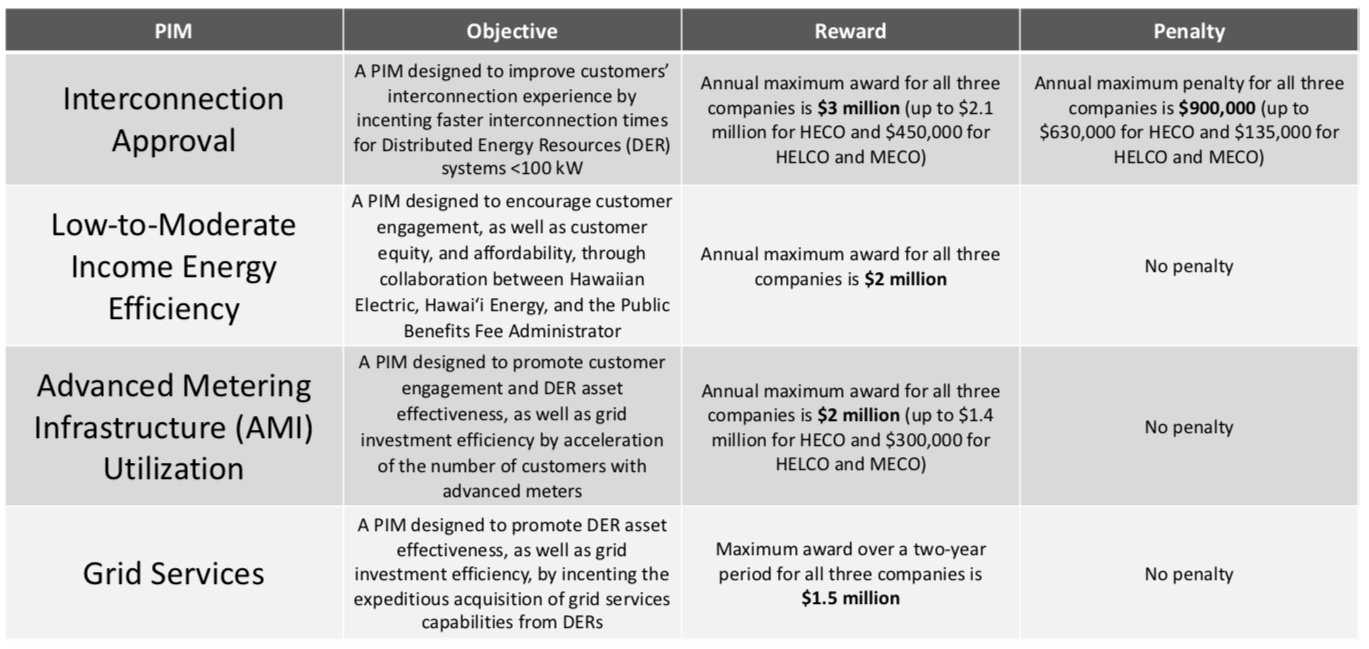

Compared to this sea change, the decision’s other new PIMs — designed to reward more effective low- and moderate-income customer energy efficiency efforts, faster smart meter deployment and distributed energy interconnection, and more effectively integrate distributed energy resources (DERs) into grid planning — offer smaller revenue boosts than the RPS-A.

Even so, they could collectively yield about $40 million over five years if HECO meets their top targets. Just how much revenue upside they’ll offer must await a series of workshops expected to yield a final decision in June, however, as regulators, HECO and stakeholders hash out the details.

(Image courtesy of the Ulupono Initiative)

HECO’s Jim Kelly wrote that the revenue upside potential built into the decision’s PIMs is “reasonable and provides us with the right incentives to aggressively move ahead with modernizing our company and Hawaii’s energy system.” At the same time, he added, “it does heavily incentivize cost control, and we’ll have to achieve a certain level of PIM rewards to offset the cost-control reductions.”

Robert Harris, public policy director at Sunrun, the leading U.S. residential solar installer and an early entrant into Hawaii’s emerging market for DERs to meet grid needs, noted that solar companies have concerns that the incentives in the decision “may not be enough to drive significant change.” On the other hand, their cumulative impact, coupled with the PUC’s signals that cost-of-service ratemaking won’t be coming back, “may create a sufficient carrot-and-stick situation.”

“We've already seen some positive steps in the right direction on solar interconnections,” he wrote in an email. “The key will likely be the commission staying heavily engaged over the next few years to ensure positive momentum.”

Fei Wang, grid edge research manager at Wood Mackenzie and author of a 2019 report on U.S. performance-based ratemaking, highlighted the importance of following through on performance incentives, which has been the step that similar efforts in the 19 states engaged in them have been reluctant to embrace.

Rhode Island, the other state that’s instituted PIMs for utility National Grid, eventually narrowed down a list of seven PIMs to one — a performance incentive on system efficiency as part of the state's power sector transformation vision and implementation plan — that is tied to financial rewards, she noted.

In that light, Hawaii is “definitely ahead of everyone else,” she said. “I wouldn’t be surprised if this is used as a blueprint for other utilities.”

But the final proof must wait for the state's utility commission to set the measures by which HECO’s progress on resolving final details of several PIMs in its post-decision working group, she said. Open questions remain on how that process will define the advanced rates and programs enabled by smart meter rollouts, for example.

“This is just a starting step,” Earthjustice’s Moriwake agreed. “But the PUC focused on some innovative emergent outcomes — and they took the lead in some innovative and proactive outcomes going forward.”