For many in the PV industry, the term "shakeout" conjures up not-so-fond memories of the winter of 2008. The reverberations of the global financial crisis and the difficulty in filling a Spain-sized hole led to a sharp drop-off in global demand, and the resulting oversupply and precipitous price drops led both market participants and pundits to foresee an apocalyptic future for many PV manufacturers. A shakeout ('consolidation' to the politically correct), they said, was arriving, and layoffs, restructurings, acquisitions, and insolvencies were on their way. Many of the more than 250 wafer, cell, and module firms around the globe would simply be unable to survive in the brutally competitive dynamic that would surely ensue, leaving behind a leaner, fitter supply chain. To quote GTM Research's own words circa January 2009: "What will likely emerge...is a substantially smaller list of companies with relatively higher concentrations, and a trimming of the overall capacity amounts to match real market demand".

Fast forward a year and a half. Have the prophecies come true? No doubt, almost every PV manufacturer had to endure severe hardship for the first half of 2009. Prominent firms have felt the heat of significant restructuring and layoffs (Q-Cells, REC, Solon, BP, United Solar). Consolidation of sizable proportions has taken place across the value chain (MEMC's acquisition of SunEdison, First Solar's acquisition of Nextlight and Optisolar pipelines, the entry of cell and wafer manufacturers into module production). And the prophecies of untimely demise have indeed come true for noteworthy firms and facilities (Applied's Sunfab business, customers Signet and Sunfilm, BP's and GE's plants in Spain and Delaware, respectively).

But truth be told, much worse was expected back then. Barring these rather notable exceptions, most PV manufacturing firms have survived, and have continued to possess essentially the same shape and form, business model-wise, as they did back in 2008. Far from thinning, the number of firms in the fray, both in crystalline silicon as well as thin film manufacturing, has only increased. Many firms that were thought to be uncompetitive are alive and well today (German module manufacturers Schott, Solar-Fabrik, Centrosolar, Aleo Solar are representative examples), and have been running at close to full utilization for the better part of the last twelve months. Overall, the industry still looks much the same as it did back in 2008. What was expected to be a quake of transformative proportions has felled only a few weak buildings and merely disturbed the furniture of most others; the city, however, still looks much the same as it did before.

So what happened? Why was the consolidation that took place only a pale shadow of what was predicted? Why are mostly all the high-cost manufacturers still around today? And what does this tell us about the future?

The Thesis

Crudely put, the 'bloody shakeout' thesis of 2009 was formulated on three basic principles: (1) demand in 2009 would remain flat or fall relative to 2008 for exogenous reasons (i.e., the evaporation of 2.5 GW of Spanish demand due to policy changes and the availability of debt capital for project finance), meaning that the size of the solar pie would not grow meaningfully; (2) manufacturing capacity, on the other hand, would continue its strong historical pattern of growth, meaning that there would be much more competition for this pie; and (3) PV was now essentially a commodity, and thus, demand for it was increasingly a function of a single variable (i.e., price/cost), meaning that high-cost manufacturers, try as they might, would simply be unable to sell product in a commoditized, demand-constrained environment.

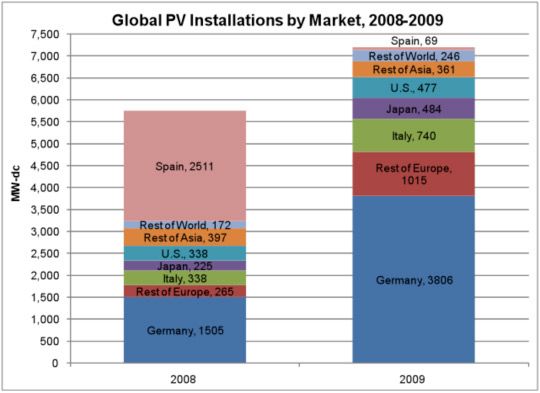

As is well known, the first of these suppositions (that demand would not grow meaningfully) has turned out not to be true. Over 7 GW of PV was installed in 2009, a healthy 25% more than the 5.6 GW in 2008. The overwhelming majority of this growth was driven by Germany, where installations grew by an astonishing 2.3 GW, or 153 percent. Quite simply, feed-in tariffs in Germany (as well as in Italy and the Czech Republic) remained generous enough to drive attractive rates of return and certainty of debt repayment for PV projects -- even those using expensive $2.00/W-plus modules (aided no doubt by successful and significant cost reduction efforts on the BOS side, as well). Looming FIT policy uncertainty in 2010 and the return of project financing in the second half of 2009 then combined to drive an unprecedented volume of German installations for the remainder of the year. With project economics still working in their favor and established low-cost players (First Solar, Suntech, Yingli, Trina) being capacity constrained, high-cost manufacturers became beneficiaries of Germany's late surge, and this state of affairs has continued well into 2010 thus far.

Still, though, if one were to examine data on manufacturing capacity (which speaks to the second point referenced above), it is difficult to understand why there should have been any business at all for less competitive manufacturers, even if the economics make sense. A cursory look at the figure below confirms that the PV market has been in a state of quite significant overcapacity through 2009; compared to 2008, where available module supply and demand were relatively well balanced (a difference of 28%, not accounting for yields and downtime), 2009 witnessed a yawning gap -- of the order of 46% -- between supply and demand. So the pundits certainly were not wrong on this front; even the most aggressive German demand ramp would not be sufficient to consume existing capacity, and it naturally follows that someone had to be doing the suffering. As it turns out, the brunt was borne not by high-cost European manufacturers, but rather by China- and Taiwan-based crystalline and amorphous silicon producers, many of whose cost structures were undoubtedly superior.

Perhaps we were mistaken in assuming that cost was everything to buyers of modules (premise #3). Perhaps other factors, such as proximity to local demand, existing sales relationships, or the cachet of "made in Europe" labels, played a more important role in determining demand than was thought. But vendor-specific installation data from both local and global markets do not substantiate these claims. As shown below, Asian manufacturers have made significant gains as regards their share of California Solar Initiative applications over the last year, from only 14 percent in Q2 2009 to a staggering 56 percent in the first quarter of 2010. As detailed in our recently published research note (free for download here), the same holds true in the global market as well, where Chinese and Taiwanese manufacturers made up 40 percent of module sales in 2009, compared to only 21 percent for higher-cost European producers. The adoption of contract manufacturing models in low-cost locations (Mexico, China, Eastern Europe) for module production by established Western producers (Q-Cells, BP, SunPower, Evergreen) only lends further credence to the argument that modules are increasingly viewed as fungible goods; beyond a point it doesn't matter where they are made or who makes them.

Bankability: The Missing Piece

So the question remains: why do installers and developers continue to purchase modules from high-cost producers (thus enabling the continuation of status quo business models) when there is an abundance of less expensive options on the market? And why do we keep hearing about the global market being in a state of module undersupply right now when available supply still exceeds demand?

The answer lies in the much-discussed but seldom explicated notion of bankability as it applies to module vendors. In a post-Lehman world, lenders have become extremely selective about which projects they choose to finance; the projects that receive capital are those with the lowest perceived risk profiles. Since the cost of debt is fixed, there is little upside for a bank if cheaper (and thus higher-return-enabling) modules are used, as long as the project clears its hurdle rate. This means only established firms with proven technologies and long-term product performance (i.e., module yields) will make the cut from the abundance of available options. It comes down to this: each lender has a relatively small, carefully chosen list of module vendors it is willing to finance (perhaps 100 in Europe, and as few as 10 in the U.S.). Unsurprisingly, almost every European crystalline silicon-based producer is on the list. Very few Asian and thin film firms currently are.

The effects are easy to understand. Essentially, the bankability factor has restricted the field of available producers to a much smaller pool; those firms that are not considered bankable are effectively shut out of the market. Indeed, this is exactly why the current market is considered to be undersupplied: as shown below, there is no shortage of module capacity, but rather of bankable module capacity. Bankability is the missing piece of the puzzle, and combined with Germany's ability to absorb high-cost modules, it is what has thus far insulated established, high-cost manufacturers from the twin effects of oversupply and commoditization.

2011: The Return of the Shakeout

This is the reality in which we find ourselves today. The lingering question, then, is to what extent this state of affairs is sustainable.

Can Germany continue to prop up high-cost manufacturers? Judging from the slew of FIT cuts that is on the way, decidedly not. After the usual mind-numbing speculation, it has been decided that tariffs will be retroactively cut by eight percent to 13 percent in July, followed by an additional across-the-board cut of three percent in October. As if this wasn't enough, there will be another reduction of 12 percent to 13 percent at the beginning of 2011. It is difficult to believe that most producers will be able to reduce costs in line with the net reductions slated to go into effect between now and Q1 2011, and consequently, that projects using high-cost modules will be viable. Also, there will be limited room for margin reduction on the BOS and project development side; they will have been squeezed tightly enough by then. And given that 2010 installations in the country will be around twice the 3-to-4-GW range policymakers have targeted, it wouldn't be surprising if more mid-year cuts were announced in 2011, as well. Thus, high-cost manufacturers will no longer be able to depend on spillover from robust German demand as in 2009 and 2010.

Is there another large market with the potential to serve as a refuge for high-cost manufacturers in 2011? In other words, if Germany is headed toward becoming the new Spain, who can be the new Germany? In its capacity to single-handedly rescue the industry, Germany stands alone in possessing that rare combination of qualities -- an uncapped market, generous subsidies, and short project-cycle times. Italy and the U.S. are the strongest candidates, but the former has laboriously long cycle times and is itself headed for a 20 percent reduction in subsidies next year (and counterintuitively, actually experiences lower module prices than Germany), while the latter is an intensely competitive, price-sensitive market.

What of the bankability factor? Could that still save the day and maintain the status quo as it pertains to the state of the PV market? Well, there are three things to consider here. First, 2010 will witness a huge jump in bankable, low-cost Chinese crystalline silicon manufacturing capacity, to the tune of over 4 GW. To the extent that this capacity needs to be utilized in 2011, we could see even larger price drops than subsidy cuts will dictate. Secondly, bankability (or rather, lack thereof) is not a permanent, everlasting condition: over time, an increasing number of companies currently on the wrong side of that line, both c-Si and thin film, will be able to alleviate concerns of risk surrounding their balance sheets and products. And thirdly, bankability doesn't really matter if you can't drive the desired return.

In summary, the unrelenting, prolonged shakeout that was originally predicted for 2009 seems increasingly likely to manifest itself beginning in early 2011. All signs point to a period of severe upheaval (i.e., restructurings, acquisitions, insolvencies) for high-cost manufacturers; unlike in 2009, however, there will be no Germany to step in, and no quick respite or return to the status quo. To survive, these firms will have to undergo significant transformation as far as their business models are concerned. Those that resist change will likely be pushed out of the market -- and this time, there will be no turning back. The next logical question is what exactly these firms can do to ensure their survival, but that's a topic for another day. For now, just don't say you weren't warned -- twice.