As Michael Kanellos reported, recent greentech IPOs have had mixed and less than stellar results. And we've looked at many of the greentech IPO prospects in the past.

The public market regurgitated Solyndra, unable to squeeze that debt level and fragile value proposition down its craw. The shiny bolus of Tesla has been swallowed, although that firm's value proposition has not been fully digested or priced.

I'll stop with the alimentary metaphors for now.

Here's a rundown of Greentech IPOs that have already priced or been withdrawn, the ones currently on deck with their S-1s filed, and some wild prognostications about who the next IPO candidates might be.

If there's a running theme here, it's that this first crop of Greentech IPOs has stunk up the room -- but there are likely some higher-quality IPOs to come.

Withdrawn Greentech IPOs

- Trony Solar just withdrew its planned IPO, about six months after the Shenzen, China-based PV module maker postponed its original IPO plans. J.P. Morgan Chase & Co. and Credit Suisse Group were the lead underwriters for the amorphous silicon solar panel vendor. Investors included Intel, which owned about 5 percent of the firm.

- Solyndra, recipient of $1 billion in VC and $500 million in government loan guarantees, could not convince institutional investors that their manufacturing costs could keep up with the solar market leaders or that profitability was remotely achievable in the near- to mid-term. We haven't heard the last of Solyndra, but it might be a while until they can try the public markets again.

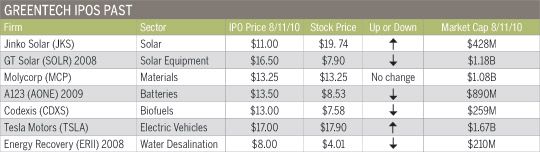

Greentech IPOs Past: Only a Few Winners

(stock prices as of 8/11/10)

If the mark of success is in exceeding the IPO strike price -- then only Tesla and Jinko meet that test.

- It's too early to tell with Tesla -- they have first mover advantage and certainly the stock will be volatile in the coming year. Let's check back in a year when hybrids and EVs from Chevy, Nissan, BYD, Hyundai, Fisker, Porsche (more Porsche here), Mercedes, BMW and VW start to reach the market.

- A123 has its share of challenges ahead. The firm just announced that it lost Chrysler as a customer and missed its revenue estimates. And recent news of spinning out a flow battery subsidiary doesn't seem like a vote of confidence for lithium-ion in large-scale utility storage applications.

- GT Solar's most recent quarter was mostly positive with earnings beating estimates, a very healthy backlog of $1.1 billion and good visibility into 2011 for the solar manufacturing equipment vendor.

Greentech IPOs Present - SEC documents Filed

- Last week saw paperwork for the proposed $200 million offering from biofuel player PetroAlgae. The firm actually no longer grows algae (it grows lemna or duckweed) and has no intention of supplying petroleum, despite their name. The company has a technology licensing business plan, zero dollars in revenue and a management team with a spotty record. It's only operation is a small-scale demo facility in Florida. In a questionable algae biofuels market, PetroAlgae is not the company to inspire confidence in institutional investors. Here's the S-1. Prediction: IPO withdrawn "because of market conditions."

(GTM Research has a research report on third and fourth generation biofuels here).

- SemiLEDS is an LED chip and component manufacturer that filed its S-1 registration this week. According to the filing, the company is looking to raise $172.5 million from the offering. The firm builds blue, green and UV LED chips for general lighting applications, including street lights and commercial, industrial and residential lighting. The company had $24.275 million in revenues and -- get this -- $6.3 million in profit in the nine months ending May 31, 2010. That's up from revenues of $7.01 million and losses of $2.707 million for the same period last year. It's the only profitable company on this list.

- Fallbrook Technologies of San Diego, a startup building an innovative transmission for vehicles and wind turbines, filed for a $50 million IPO back in February. Here's their S-1. Fallbrook has developed a transmission that improves the efficiency and performance of mechanical systems that run at different speeds between primary drive and operating drive. Here's a link to a video that explains their technology. The startup identifies several multi-billion dollar markets for its NuVinci transmissions: automotive accessory drives, bicycles, electric vehicles, etc. Fallbrook claims its transmission improves EV battery life and increases operating range in applications such as lawn care equipment and small wind turbines. The firm has received $55 million in venture funding since its founding in 2000 and its largest shareholders are NGEN and Robeco. This might be a tough sell to institutional investors.

- Amyris feeds sugars to custom microbes, which in turn exude hydrocarbons that are then converted to fuels or industrial chemicals. The first product out of the company was an artificial version of artemisinin, an antimalaria drug that drew millions in support from the Bill and Melinda Gates Foundation.

- Here are the real kickers in the list of investment risks: The company has no experience producing products at the commercial scale, they have no production agreements, they have a limited operating history and have not generated revenues from the sale of any of their renewable products. To date, their revenues have consisted of sales of ethanol produced by third parties, funding from third-party collaborative research services and government grants. That would make them a distributor -- a money-losing distributor. And a grant mill.

- The company had 2007 sales of $6.1 million, 2008 sales of $13.9 million and 2009 sales of $64.6 million. The company lost $11.7 million in 2007, $41.8 million in 2008, and a whopping $64.4 million in 2009. To date, Amyris’ cumulative deficit stands at $120.4 million.

- The company genetically modifies microorganisms, primarily yeast, and uses them "as living factories in established fermentation processes to convert plant-sourced sugars into potentially thousands of target molecules." Their first commercialization efforts have been focused on a molecule called farnesene, the basis for a range of products varying from specialty chemical applications such as detergents, cosmetics, perfumes and industrial lubricants, to transportation fuels such as diesel.

- Here's the link to the S-1. The synthetic biology firm has raised more than $244 million in private funding from Kleiner Perkins Caufield & Byers, Khosla Ventures, TPG Biotechnology, Advanced Equities, DAG Ventures, Grupo Cornélio Brennand, Naxos Capital Partners, The Westly Group, Stratus Group, and Temasek Holdings, et al. and is looking to raise $100 million. (GTM Research has a research report on third and fourth generation biofuels here).

- Biobutanol producer Gevo is looking to raise up to $150 million led by underwriters UBS Investment Bank, Goldman Sachs, and Piper Jaffray. Here's a link to the S-1. Gevo has raised more than $40 million in funding from Burrill & Co., Malaysian Life Sciences Capital Fund, Khosla Ventures, Lanxess and Virgin Green Fund. Khosla Ventures is the leading share holder at more than 40 percent.

- Gevo had a mere $660,000 in revenue in 2010 -- hardly IPO material. Until this month, that is, when Gevo acquired 18-million-gallon-per-year ethanol producer Agri-Energy. With that acquisition, Gevo suddenly has $40.7 million in revenue, with losses of $18.2 million. Gevo is working on a fermentation process to produce isobutanol from the fermentable sugars in cellulosic biomass. Isobutanol is a building block for making biodiesel, jet fuel and other materials. The S-1 estimates the global market for isobutanol as more than a trillion gallons per year. (GTM Research has a research report on third and fourth generation biofuels here.)

- Gevo's strategy, according to their S-1, "is to commercialize biobased alternatives to petroleum-based products using a combination of synthetic biology and chemical technology." They "intend to produce and sell isobutanol, a four carbon alcohol. Isobutanol can be sold directly for use as a specialty chemical or a value-added fuel blendstock. It can also be converted into butenes using simple dehydration chemistry deployed in the refining and petrochemicals industries today. Butenes are primary hydrocarbon feedstocks that can be employed to create substitutes for the fossil fuels used in the production of plastics, fibers, rubber, other polymers and hydrocarbon fuels. Customer interest in our isobutanol is primarily driven by its potential to serve as a building block to produce alternative sources of raw materials for their products at competitive prices."

- Rob Day refers to this IPO as a venture capital/project finance fundraising and "not your classic IPO liquidity event" -- along with some more insight here.

And Future: Top Ten Greentech IPO Hopefuls

Here's where it gets interesting. Unlike most of the previously listed (and frankly, rather questionable) firms, the list of companies to follow actually have real products, serious revenue and the prospect of profits in high-growth markets. Here's a list of ten potential greentech IPOs coming in late 2010 through 2012:

Bloom Energy has a great story, revenue from the sales of its Bloom Boxes and marquee customers including Cypress, Google, FedEx and San Francisco's SFO Aiport. The company's Solid Oxide Fuel Cells (SOFCs) are an alternative to diesel gen-sets in the off-grid world and to the electric grid in the developed world. The fuel cells run on natural gas which, in the view of some, makes the value proposition fragile. But a strong team, veteran investors and a big narrative make this a firm to watch, profitability and value proposition notwithstanding.

Bridgelux has emerged from the pack of LED startups with a solid product roadmap and a CEO (Bill Watkins) familiar with the scale-up issues surrounding tech companies. The firm is aiming at the commercial market, avoiding the coming residential bulb bloodbath. Still, Bridgelux must compete against Philips, Osram, GE and other companies with over 100 years of experience and mature sales channels all over the world. Reliable sources at the Director level inform us that revenue is in the high tens of millions.

BrightSource Energy is the leader in the solar thermal startup world, now that the Ivanpah CSP plant has been given the green light. That's hundreds of megawatts of power under contract and gigawatts of power in the pipeline. An enormous $1.37 billion federal loan guarantee has been won and investors, developers and EPC personnel are in place. But revenue doesn't flow until power flows, which explains why the company is looking at Thermal Enhanced Oil Recovery (TEOR) as a shorter term revenue source.

Enphase has shipped more than 300,000 of their microinverters, carved out more than a 10 percent U.S. market share in Q1, according to the CEO, and has a strong balance sheet -- partially from a recent funding infusion from Kleiner Perkins. The inverter and microinverter market is growing fast and Enphase is the microinverter leader. Reliability issues seem to have been addressed, although gross margin questions remain. The company has made a tentative foray into the consumer-facing smart grid with an automated thermostat, looking to leverage their platform into other markets.

Intematix produces a product that makes LEDs work. Their phosphor materials enable LEDs for general illumination to achieve good quality light and efficiency. Reliable sources indicate that the company is generating revenue in the "tens of millions." What's more, the LED lighting market seems to be poised at an interesting tipping point.

OPower is an energy efficiency company focused on customer engagement and behavior modification, currently providing millions of homes with in-home energy data and efficiency advice via paper reports or online. The platform is described as advanced customer engagement. The firm says about 85 percent of their customers will cut power consumption by around 3.5 percent. The customized data lets people know much energy they're using in comparison to their neighbors and then follows it up with a recommended course of action to maximize energy savings. Revenues exceed $30 million according to sources at the firm.

Serious Materials has yet to build a commercial-scale factory for its green drywall, but is selling tens of millions' worth of thermal windows. Rumors are that it will try next to move into other markets for building products, such as insulation and home management controls. CEO Kevin Surace has talked about this for years, and an IPO would give him the cash to expand. 2009 revenue was reported in the $50 million range.

Silver Spring Networks' S-1 filing is rumored for the fall of this year. Silver Spring has won multimillion dollar contracts in California, Texas and Australia for the mesh networking systems that connect meters to utilities. They've hit a few speed bumps with the PG&E smart grid backlash and there are profitability concerns, but the revenue bar seems to have been reached to allow serious consideration of the public offering.

Solar City has raised $60 million in tax-equity financing from PG&E, a $90 million fund with U.S. Bancorp and the backing of premier VCs. The firm started its existence looking to add efficiency to the solar installation process. It then moved into financing and leasing the solar systems for residential rooftops, and it has just added energy efficiency services to its competencies through its acquisition of Building Solutions. It has significant revenues from its operations in Arizona, California, Colorado, Oregon and Texas, but, like other service industries, the company is faced with the challenge of how to efficiently and profitably scale the business.

Suniva, as reported by GTM Research analyst Shyam Mehta, began commercial production of its monocrystalline cells in late 2008, and "unlike many struggling PV startups that entered the market around that time, the company has gone from strength to strength over the last 18 months," with "one of the quickest production ramps of any Western PV company." Suniva went from an initial 32 megawatts to 96 megawatts to a current 170 megawatts of cell capacity, and is sold out for 2010. The company has its own paste and texture recipes, is able to customize and optimize every layer of the cell design to its own specifications, and has leveraged its considerable R&D experience to optimize each processing step to a high degree. While Suniva is clearly not going to overtake SunPower or Sanyo any time soon, reports suggest that the company has a much better cost structure compared to these two players, one that is more in line with low-cost manufacturers. That, combined with its current efficiency advantage over other firms, makes it competitively positioned for right now. A 19-percent efficiency cell is in the works and that should help the firm maintain competitiveness in the near future, as well. "The key question is whether the company can maintain this advantage going forward, given that major Chinese players are hell-bent on playing catch-up," according to Mehta.

***

Michael Kanellos contributed to this article.